So, you’re thinking about buying a house, huh?

Look, I get it. Purchasing a home is probably one of the biggest financial moves you’ll ever make. It’s exciting, terrifying, and honestly? A little overwhelming. Before you sign on that dotted line and commit to decades of payments, you really need to understand the ABCs of a mortgage. Trust me on this one – mortgage amortization isn’t just some boring financial jargon. It’s actually the secret sauce that’ll help you save thousands of dollars and maybe even retire early. (Okay, maybe not retire to a private island, but you get what I mean.)

Here’s what we’re gonna cover today:

First off, there’s way more to a mortgage than just the amount you borrowed and the interest you’ll pay. There’s this whole behind-the-scenes system called mortgage amortization that structures how you’ll pay back your loan over time. And here’s the cool part – once you understand how it works, you can actually game the system a bit. Making extra principal payments can literally save you thousands in interest charges and help you build equity in your home way faster. Plus, understanding all this stuff helps you balance your housing costs with other important money goals, like actually having a retirement fund and not living paycheck to paycheck.

What I’m hoping to do here is help you put this whole mortgage puzzle together. I want you to understand how everything works, and then I’ll give you some practical tips for managing your payments without feeling like you need a PhD in finance.

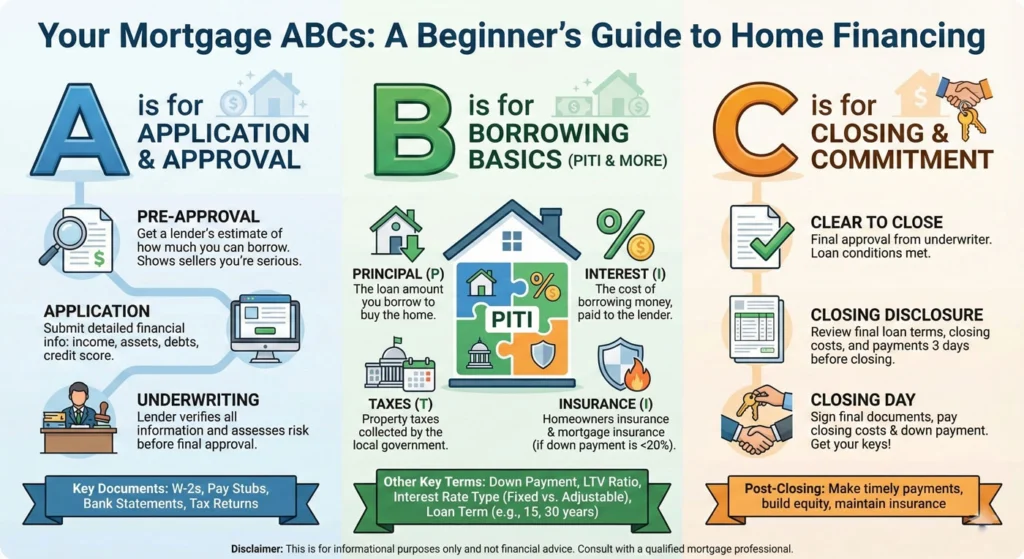

- The Five Essential Components of Your Monthly Mortgage Payment (P.I.T.I. + T)

- Understanding Mortgage Amortization Schedules

- Accelerated Payoff Strategies and Financial Planning

- Leveraging Data and Calculators for Smart Decisions

- Real-World Examples: How People Actually Get Mortgages

- Case Study 1: Nick the Contractor – When Your Income Doesn't Fit the Box

- Case Study 2: Emmanuel the Agency Worker – Making It Work with 95% LTV

- Case Study 3: Jessica Smith – When One Mistake Comes Back to Haunt You

- What These Case Studies Really Tell Us

- Frequently Asked Questions

- What is the difference between Amortization Period and Mortgage Term (Canada)?

- What is Mortgage Amortization?

- What is the maximum amortization period allowed in Canada?

- Does making extra payments actually save money?

- Conclusion: A Data-Driven Path to Financial Freedom

The Five Essential Components of Your Monthly Mortgage Payment (P.I.T.I. + T)

Alright, let’s break down what you’re actually paying for each month. Spoiler alert: it’s more complicated than you’d think.

Principal: The Core Debt

So, the principal is pretty straightforward – it’s just the actual money you borrowed from the lender. If you bought a $300,000 house and put down $60,000, your principal is $240,000. Simple enough, right?

Here’s why this matters: every dollar you pay toward the principal is actually building equity in your home. That’s YOUR money, not the bank’s. Financial experts (the smart folks who actually know what they’re talking about) always recommend making extra payments directly to your principal balance when you can. It’s like a cheat code for paying off your loan faster and reducing how much interest you’ll pay overall.

Interest: The Cost of the Loan

Okay, now for the not-so-fun part. Interest is basically the fee your lender charges you for taking the risk of lending you hundreds of thousands of dollars. Can’t really blame them, I guess.

Here’s the thing – your credit score is HUGE when it comes to your interest rate. The better your credit, the lower your rate. We’re talking potentially tens of thousands of dollars in savings over the life of your loan. So yeah, maybe don’t max out those credit cards before applying for a mortgage, okay?

One silver lining (at least if you’re in the US): mortgage interest is tax-deductible up to a certain amount if you itemize on your tax return. It’s not exactly fun money, but hey, at least Uncle Sam gives you a little break.

Taxes and Escrow

Alright, so here’s where things get a bit more complicated. Most lenders will set up something called an escrow account. Think of it like a savings account that your lender manages for you to pay your property taxes and homeowners insurance.

The cool part? You don’t have to worry about remembering to pay these bills or scrambling to come up with a huge chunk of money once or twice a year. It’s all rolled into your monthly mortgage payment, and the lender handles everything. No penalty fees, no coverage gaps, no stress.

Some people opt out of escrow to lower their monthly payments, but honestly? Unless you’re really disciplined with budgeting, I’d stick with it. Future you will thank present you for not having to deal with a massive tax bill.

Insurance (Homeowners and PMI)

Insurance is one of those necessary evils. Homeowners insurance is required in pretty much every state, and for good reason – you need to protect your investment.

Now, here’s where it gets annoying. If you’re putting down less than 20%, you’ll probably need to pay for Private Mortgage Insurance (PMI). And here’s the kicker – PMI protects the LENDER, not you. Feels a bit unfair, doesn’t it? The good news is you can get rid of it once you hit 20% equity in your home.

Can’t swing a 20% down payment? No worries. Some homebuyers go with an FHA-backed mortgage and put down as little as 3.5%. It’s not ideal because you’ll have insurance costs, but it gets your foot in the door of homeownership.

Term: The Repayment Length

The term is just how long you have to pay back the mortgage. Most people go with 15, 20, or 30 years.

Here’s the trade-off: shorter terms mean your monthly payment is higher, but you’ll pay way less interest overall. Longer terms mean smaller monthly payments that are easier to manage, but you’ll end up paying a LOT more in interest over time. It’s like choosing between ripping off the Band-Aid quickly or slowly – both hurt, just in different ways.

Understanding Mortgage Amortization Schedules

Okay, this is where things get interesting. Ready?

What is Amortization and How Does the Payment Structure Change?

So, mortgage amortization is basically the process of paying off your loan over time with regular payments. Each payment covers both the principal (what you borrowed) and the interest (what it costs you to borrow it).

Here’s the wild part: at the beginning of your loan, when you still owe a ton of money, most of your monthly payment goes toward interest. Like, a ridiculous amount. It can feel pretty discouraging when you make that first payment and realize only a tiny fraction went toward your actual loan balance.

But don’t worry – it gets better! As you keep making payments and your balance decreases, less interest builds up each month. That means more and more of your payment starts “chipping away” at the principal. By the end of your loan, you’re basically just paying off principal with barely any interest.

It’s like watching a really slow transformation. Patience is key here.

Key Elements of an Amortization Schedule (Table)

An amortization schedule is basically a super detailed table that shows every single payment you’ll make over the life of your loan. It tells you exactly how much goes to principal, how much goes to interest, and what your remaining balance will be after each payment.

To create one, you need:

- Your loan amount

- Your interest rate

- Your loan term (in years)

- Your loan start date

Here’s what you’ll see in the schedule:

| What You’re Looking At | What It Means |

|---|---|

| Period/Date | Just the payment number and when it’s due |

| Interest Paid | How much of your payment went to interest (this decreases over time – yay!) |

| Principal Paid | How much actually went toward your loan balance (this increases over time – double yay!) |

| Remaining Balance | How much you still owe after making the payment |

Amortization with Different Loan Types

Not all mortgages are created equal, folks.

Fixed-Rate Mortgages: These are the straightforward ones. Your principal and interest payment stays the same for the entire loan. The ratio of principal to interest changes (remember that shift we talked about?), but your payment doesn’t. The amortization happens once at the beginning, and that’s it.

Adjustable-Rate Mortgages (ARMs): These are trickier. You get a fixed rate at first (maybe 5-7 years), then it becomes variable and changes based on market conditions. Every time your rate adjusts, your lender recalculates your amortization schedule, which means your monthly payment can change. It’s like playing financial roulette.

Negative Amortization: This is the scary one. This happens when your monthly payment doesn’t even cover the interest you owe. The unpaid interest gets added to your loan balance, so you actually end up owing MORE than you borrowed. Avoid this at all costs, seriously.

Accelerated Payoff Strategies and Financial Planning

Alright, now for the good stuff – how to pay off your mortgage faster and save a boatload of money.

High-Impact Methods to Pay Down Principal Faster

1. Make Extra Principal Payments

This is the simplest hack in the book. Any extra money you send toward your principal reduces the amount that interest is calculated on. Even small amounts add up over time. Got a bonus at work? Tax refund? Throw some of it at your principal. You’ll cut years off your loan and save thousands in interest.

2. Bi-Weekly Payments

Here’s a clever trick: instead of making one monthly payment, pay half your mortgage amount every two weeks. You end up making 26 half-payments per year, which equals 13 full payments instead of 12. That one extra payment per year can shave almost 5.5 years off a 30-year mortgage. A mortgage amortization calculator can show you exactly how much you’d save.

3. Refinance to a Shorter Term

If you can afford higher monthly payments, refinancing from a 30-year to a 15-year mortgage can seriously accelerate your payoff. You’ll pay way less interest overall, though you’ll have closing costs to deal with. (Quick note for my Canadian friends: if you need mortgage insurance, the longest amortization allowed is 25 years up there.)

4. Recast the Mortgage

Got a lump sum of cash? You can pay it toward your principal and ask your lender to recalculate your amortization schedule. Your interest rate stays the same, but your future monthly payments drop. It’s like a mini-refinance without all the hassle and costs.

Balancing Mortgage Payoff with Broader Financial Goals

Listen, I know you’re excited about paying off your mortgage early, but let’s be smart about this.

Get rid of high-interest debt first. If you’ve got credit card balances or payday loans (please tell me you don’t have payday loans), tackle those before aggressively paying down your mortgage. Those interest rates are probably way higher than your mortgage rate.

Build an emergency fund. This is non-negotiable. You need at least three to six months of expenses saved up for when life throws you a curveball. And trust me, it will.

Don’t forget about retirement. Compound interest is magical, especially when you’re young. If your mortgage interest rate is relatively low (like 3-4%), you might be better off investing extra money in your 401(k) or IRA instead of throwing it all at your mortgage.

Consider the tax implications. If you’re itemizing deductions and benefiting from the mortgage interest deduction, paying off your loan early means losing that tax break. Do the math before making big decisions.

Leveraging Data and Calculators for Smart Decisions

Let’s talk tools, because this is the 21st century and we don’t have to do math by hand anymore.

The Role of Amortization Calculators

A mortgage amortization calculator (sometimes called a loan schedule calculator) is your new best friend. These things are amazing for visualizing your payoff process and comparing different scenarios.

You can plug in different interest rates, add extra payments, test out different amortization schedules – basically play around with all sorts of “what if” scenarios. Want to see how much you’d save by paying an extra $100 per month? The calculator shows you instantly.

The best calculator really depends on what you need. If you’re in Canada, Ratehub is supposedly the top overall choice for determining affordability and calculating payoff scenarios. For the amortization formula for mortgage calculations, there are tons of free online tools – just Google “mortgage amortization calculator” and take your pick.

Applying Data Science and Analytics to Personal Finance

Okay, this might sound fancy, but stay with me.

Data literacy is your superpower. Understanding how to read and interpret financial data helps you tell good advice from terrible advice. It gives you confidence in your decisions.

Data science is basically collecting and organizing your financial information. Track your expenses, identify patterns (like “wow, I spend way too much on takeout”), and structure your data into categories like fixed expenses versus variable ones.

Data analytics takes that organized information and turns it into wisdom. You can budget better, forecast your cash flow, evaluate whether your investments are actually making money, and track your net worth over time.

Visualization makes everything easier. Instead of staring at spreadsheets full of numbers, turn them into charts and graphs. Trends jump out at you, patterns become obvious, and you can make decisions faster. Plus, it’s way less boring than reading through financial reports.

Real-World Examples: How People Actually Get Mortgages

Okay, enough theory. Let’s talk about real people who figured this stuff out. These case studies from the 2025-2026 housing market show that even when your situation isn’t textbook perfect, you can still make homeownership happen.

Case Study 1: Nick the Contractor – When Your Income Doesn’t Fit the Box

Nick had been working as a contractor for three years with a solid daily rate. Sounds great, right? Except when he went to get a mortgage, he hit a wall. He had two years of company accounts, but they only showed dividend draws – no formal salary, no traditional monthly payslips. Most mortgage brokers took one look and basically said, “Sorry, can’t help you.”

Here’s what saved him: He found a specialist lender (Nationwide Building Society in this case) that understood “bespoke underwriting.” Instead of obsessing over W-2s and pay stubs, they looked at his contractor day rate as proof he could afford the payments.

The Result: Nick got approved for a 90% LTV mortgage. The lesson? If you’re self-employed, a freelancer, or have non-traditional income, don’t give up after the first rejection. Find lenders who specialize in your type of situation. They exist, and they actually understand how modern work looks.

Case Study 2: Emmanuel the Agency Worker – Making It Work with 95% LTV

Emmanuel was working two jobs – one as an agency worker and one as a part-time permanent healthcare employee. He wanted to buy a house but could only scrape together a 5% down payment. Most automated underwriting systems looked at his dual income streams and basically short-circuited.

But Emmanuel found a regional building society that did manual underwriting. An actual human being looked at his application and said, “Okay, let’s combine both income sources and see if the numbers work.”

The Result: He got his mortgage offer one month after applying and closed on his home two months later with that 95% LTV. The takeaway here? If you’ve got a 95% LTV situation or complicated income sources, regional lenders and government-backed programs (like FHA) often have more flexibility than the big national banks.

Case Study 3: Jessica Smith – When One Mistake Comes Back to Haunt You

Jessica’s situation is probably the most relatable. Back in 2020, during the height of COVID, she got laid off temporarily and missed a credit card payment. Fast forward to 2025, and that late payment was still on her credit report, threatening to derail her mortgage application.

The underwriter asked for a Letter of Explanation (LOE). Jessica didn’t just write “sorry, it was COVID.” She provided:

- Her termination letter from 2020

- Bank statements showing that once she got rehired, every payment was on time

- Proof that she’d set up automatic payments to prevent future issues

The Result: The underwriter approved her loan. They saw the late payment as an isolated incident during extraordinary circumstances, not a pattern of financial irresponsibility.

The Lesson: If you’ve got some dings on your credit report, context matters. Don’t hide from it – explain it clearly, provide documentation, and show that you’ve taken steps to prevent it from happening again. Underwriters are human (well, most of them), and they understand that life happens.

What These Case Studies Really Tell Us

Look, the 2025-2026 housing market is tough. The median credit score for purchase loans hit a record high of 768 in May 2025. Interest rates are hovering between 6.19% and 6.37%. Home prices are still elevated. It’s not the easiest time to buy.

But here’s the thing – these three people found a way. They didn’t have perfect credit or traditional employment or massive down payments. What they had was persistence, the right guidance, and lenders willing to look beyond the checkbox requirements.

If you’re in a similar situation:

- Non-traditional income? Seek out specialist lenders who understand your work situation

- Small down payment? Look into FHA, VA, or USDA loans, or find regional lenders with flexible programs

- Credit issues? Be proactive with your explanations and document everything

The mortgage “ABCs” we’ve been talking about aren’t just abstract concepts – they’re the actual framework that determined whether Nick, Emmanuel, and Jessica got approved or rejected. Understanding this stuff gives you power.

Frequently Asked Questions

What is the difference between Amortization Period and Mortgage Term (Canada)?

Great question! The amortization period is the total time it’ll take to pay off your entire mortgage – usually 20, 25, or 30 years. The mortgage term is way shorter (maybe 6 months to 5 years) and it’s basically how long you’re locked into your current contract and interest rate with your lender. When your term ends, you need to renew. Think of the amortization period as the full marathon and the term as just one leg of the race.

What is Mortgage Amortization?

Mortgage amortization is just the gradual process of paying off your loan over time through regular monthly payments. Each payment gets split between paying down what you borrowed (the principal) and paying the interest you owe. It’s like slowly chipping away at a massive ice sculpture until it’s gone.

What is the maximum amortization period allowed in Canada?

If you need mortgage insurance (usually because you have a smaller down payment), the longest you can stretch out your payments is 25 years. If you don’t need that insurance, you can go up to 30 years. The longer the amortization, the lower your monthly payments, but the more interest you’ll pay overall.

Does making extra payments actually save money?

Yes, yes, YES! Even small extra payments make a huge difference. Rounding up your payment, making one extra payment per year, throwing your tax refund at the principal – all of it helps. Because interest is calculated on your remaining balance, paying down the principal faster means you pay significantly less total interest over the life of your loan. We’re talking potentially tens of thousands of dollars in savings.

Conclusion: A Data-Driven Path to Financial Freedom

Here’s the thing about financial planning – it’s not something you do once and forget about. It’s an ongoing process that changes as your life changes. In your 20s, you might be focused on crushing student loan debt. In your 40s, retirement suddenly seems way more urgent. Life happens, priorities shift, and your financial plan needs to shift with it.

Understanding mortgage amortization isn’t just about being a finance nerd (though if that’s your thing, no judgment). It’s about taking control of your financial future. Instead of making wild guesses and hoping for the best, you can make informed, data-driven decisions about one of the biggest financial commitments of your life.

By mastering the data behind your mortgage – using tools like a mortgage amortization calculator and understanding the amortization formula for mortgage calculations – you’re setting yourself up to reach your long-term goals. Financial freedom isn’t some abstract concept reserved for trust fund kids and lottery winners. It’s totally achievable when you understand how the system works and make it work for you.

Here’s my favorite analogy: Think about mortgage amortization like watching a financial seesaw. At the beginning, the weight of your payment is super heavy on the Interest side, while Principal lifts slowly. As you keep making payments, the weight gradually shifts until, near the end of your loan, the Principal side slams down hard with almost no weight left on the Interest side. Making extra payments? That’s like placing rocks on the Principal side early, forcing that shift to happen way faster. Pretty cool, right?

So go ahead – dive into those amortization schedules, play around with calculators, and start making informed decisions about your mortgage. Your future self (and your bank account) will thank you for it.

References:

Federal Housing Finance Agency. (2024, November 26). FHFA announces conforming loan limit values for 2025. The baseline 2025 conforming loan limit for one‑unit properties is $806,500, a 5.2% increase from 2024. (fhfa.gov)

Bankrate. (2025, June 26). What credit score do you need to buy a house? Includes minimum credit score guidelines by loan type (conventional 620+, FHA from 500 with larger down payment, etc.) and cites a median credit score of 772 for new mortgages in Q1 2025 from the New York Fed, as well as the 2025 conforming loan limit of $806,500. (bankrate.com)

Federal Reserve Bank of New York. (2025). Quarterly report on household debt and credit, 2025 Q1. Provides data on credit scores of new mortgage borrowers, including median credit scores in the high‑700s for recently originated mortgages. (newyorkfed.org)

Bankrate. (2026, January 30). Mortgage rate history: 1970s to 2025. Reports that the average 30‑year fixed mortgage rate in 2025 was 6.66%, with detailed context on 2020s rate trends. (bankrate.com)

Federal Reserve Bank of St. Louis. (2026). 30‑Year fixed rate mortgage average in the United States (MORTGAGE30US). FRED data series showing weekly 30‑year fixed mortgage rates, including late‑2025 levels in the low‑6% range and 6.10% on 2025‑12‑31. (stlouisfed.org)

Experian. (2024, October 23). How have credit scores for mortgage borrowers changed? Notes that average FICO scores for mortgage borrowers have risen over time and were around 758 in Q2 2024, demonstrating the trend toward stronger credit profiles among recent borrowers. (experian.com)

FHA.com. (n.d.). FHA down payments for homebuyers. States that FHA borrowers with a FICO score of at least 580 can qualify for a 3.5% minimum down payment, while scores below 580 typically require 10% down. (fha.com)

Bankrate. (2025, August 1). How much is an FHA loan down payment? Summarizes HUD Handbook 4000.1 requirements and confirms FHA minimum down‑payment rules and FHA mortgage insurance (MIP) structure. (bankrate.com)

Fannie Mae. (n.d.). What to know about private mortgage insurance (PMI). Explains that PMI is generally required on conventional loans with less than 20% down and can usually be removed when the loan balance falls below 80% of the home’s original value, with automatic termination at 78%. (fanniemae.com)

Rocket Mortgage. (2025, December 4). What are closing costs and how much will you pay? States that buyer closing costs typically range from 3% to 6% of the loan amount, and explains common fee types and prepaid escrow funding. Also confirms that PMI is required on conventional loans with <20% down and may be canceled at 20% equity. (rocketmortgage.com)

Bankrate. (2025, September 5). What is a debt‑to‑income ratio for a mortgage? Describes front‑end and back‑end DTI, and notes that conventional guidelines often use 28% for housing costs and 36% for total debt as reference points, with maximum DTIs up to roughly 45–50% in some cases and higher allowances for FHA/VA/USDA with compensating factors. (bankrate.com)

U.S. Bank. (2025, November 10). What is an escrow account and how does it work? Explains that lenders collect 1/12 of annual taxes and insurance with each payment, deposit it into escrow, pay bills when due, and perform an annual escrow analysis to adjust for tax/insurance changes and handle shortages or overages. (usbank.com)

Financial Consumer Agency of Canada. (2020, December 29). Mortgage terms and amortization. Explains the difference between term and amortization and notes that, when the down payment is less than 20%, the maximum amortization is typically 25 years in most cases (with some specific 30‑year allowances for first‑time buyers/new builds). (canada.ca)

Internal Revenue Service. (2025). Publication 936: Home mortgage interest deduction (2025). Describes the rules for deducting home mortgage interest in the U.S., including the requirement to itemize deductions on Schedule A and the debt limits for fully deductible interest on qualified residences. (irs.gov)

Harvard Business School, Institute for Business in Global Society. (2025, August 21). Climate change is upending homeowners insurance nationwide. Discusses how increased climate‑driven extreme weather has led to soaring homeowners insurance premiums, reduced availability, and higher replacement costs, making taxes and insurance a growing share of total housing cost. (hbs.edu)

Harvard Western Insurance. (2025, February 5). $9.4B record claims: Why home insurance is rising in 2026. Details how severe weather losses in Canada (record $9.4B insured losses in 2024) and rising construction costs have driven sharp increases in home insurance premiums, especially in high‑risk regions. (harvardwestern.com)

Mortgage Bankers Association. (2025, October 19). MBA forecast: Total single‑family mortgage originations to increase 8 percent to $2.2 trillion in 2026. Notes MBA’s expectation that 30‑year mortgage rates will remain in roughly the 6.0%–6.5% range, supporting the case study’s use of mid‑6% mortgage rates in 2025–2026 scenarios. (mba.org)