Look, I get it—you want the quick answer before diving into all the details. So here’s the deal:

If you’re planning to bounce before 20 years: BRS is your winner, hands down, 100%. Why? Because you’ll actually walk away with something! The government throws matching contributions into your TSP, and that money is yours to keep. With High-3? You get zilch if you leave early. Nada. Nothing.

If you’ve already got 9-10+ years under your belt and you’re committed to hitting that 20-year mark: High-3 wins from a purely financial standpoint. The numbers don’t lie—you’ll make more money in the long run.

If you’re sitting at less than 7-8 years and planning to go the full 20: BRS might actually give you more income over your lifetime, but here’s the catch—it depends on your TSP returns being solid and you actually contributing consistently. It’s not a guarantee like High-3.

The core difference? Think of it this way: High-3 gives you a bigger, more predictable paycheck every month. BRS gives you flexibility and something to show for your service even if life throws you a curveball and you can’t make it to 20 years. And let’s be real—over 80% of folks who join the military don’t hit that 20-year mark, so BRS helps a whole lot more people.

- Understanding the Two Pillars of Military Retirement (What the Heck Are These Things, Anyway?)

- Key BRS Features and Financial Risks (The Stuff That Could Bite You)

- Retirement for National Guard and Reserves (Because You're Part of the Team Too)

- Critical TSP Rules & Investment Strategy (Don't Screw This Up)

- Maximizing Financial Health: Avoiding Common Pension Estimate Mistakes (Because Errors Happen)

- 2026 Military Pay and COLA Increases

- The Rising Cost of Retiree Healthcare (Because Nothing Stays Cheap Forever)

- Next Steps and Trusted Resources (Time to Actually Do Something)

- Understanding BRS vs. High-3: A Simple Analogy

- Final Thoughts: Your Retirement, Your Choice

Understanding the Two Pillars of Military Retirement (What the Heck Are These Things, Anyway?)

Alright, let’s get into the nitty-gritty of what these two systems actually are. I’ll keep it simple—promise.

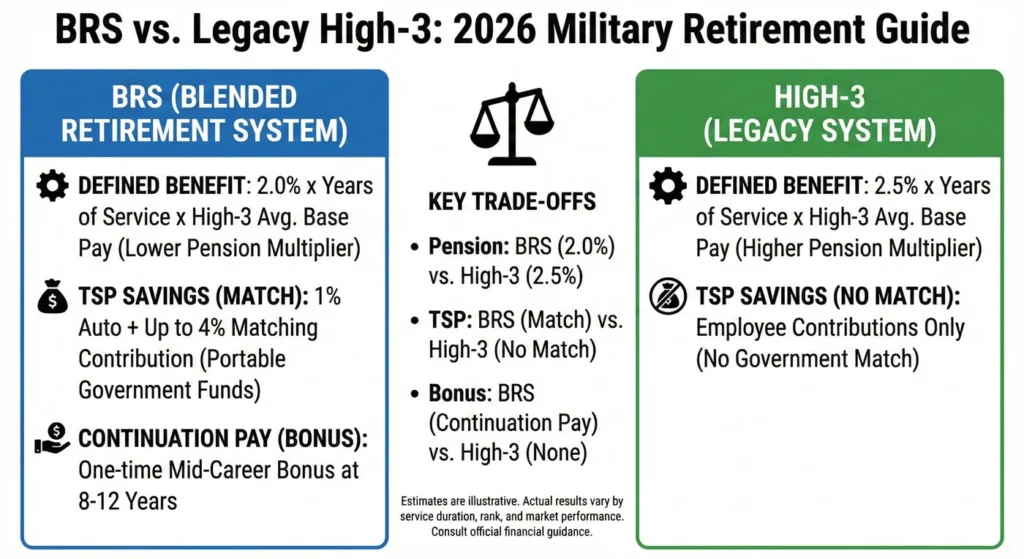

The Legacy Retirement System (High-3) Defined

This is the “old school” way of doing military retirement, and honestly, it’s pretty straightforward once you get it.

How they calculate your pension: They look at your highest 3 years (36 months) of basic pay—usually your last three years because you’re making the most money by then—and average it out.

The magic multiplier: You get 2.5% of that average for every year you serve. The math looks like this:

Monthly Pension = 2.5% × Years of Service × High-36 Average Basic Pay

So if you retire at exactly 20 years, you’re getting 50% of your highest three years’ base pay (2.5% × 20 = 50%). Not bad, right?

The 20-year payout: Yeah, so at 20 years, you’re pulling in half your base pay for the rest of your life. That’s a pretty sweet deal if you can stick it out.

TSP contributions: Sure, you can throw money into your Thrift Savings Plan (TSP)—that’s the military’s version of a 401(k)—but here’s the kicker: the government doesn’t match a single penny. It’s all on you.

The “all or nothing” problem: This is the brutal part. If you serve for 19 years and 364 days and then leave, you get exactly zero dollars in pension. You have to make it to 20 years, or you’re walking away empty-handed when it comes to that military retirement pay. This is what the policy wonks call “cliff vesting,” and it’s why 81% of service members who separate get nothing.

The Blended Retirement System (BRS) Defined

Now we’re talking about the new kid on the block. BRS launched in 2018, and it’s called “blended” because it mixes two types of retirement savings.

The “blend”: You get a traditional pension (like High-3, but smaller) PLUS the government actually matches your TSP contributions. It’s like having two retirement accounts working for you. The DoD designed this as a “four-pillar” system: the pension, TSP matching, Continuation Pay, and the lump sum option.

How they calculate your pension: Pretty similar to High-3—they take the average of your highest three years of basic pay, but here’s the difference…

The multiplier: Instead of 2.5%, you only get 2% for each year of service. The formula is:

Monthly Pension = 2.0% × Years of Service × High-36 Average Basic Pay

Yeah, I know—it sounds like you’re getting shorted, but stay with me.

Payout at 20 years: This means at 20 years, you’re only getting 40% of your highest three years’ base pay (2.0% × 20 = 40%). That’s 10% less than High-3. But remember, you’ve also got that TSP growing on the side.

TSP Government Matching (the good stuff): Here’s where BRS gets interesting. The government automatically dumps 1% of your base pay into your TSP after just 60 days of service—you don’t have to do anything. Then, after two years of service, if you contribute up to 5% of your base pay, they’ll match it dollar for dollar. That’s free money, folks! If you’re not taking advantage of this, you’re literally turning down a raise.

The Matching Breakdown (2026):

| Your Contribution | Auto 1% | Match | Total Gov’t Money |

|---|---|---|---|

| 0% | 1% | 0% | 1% |

| 1% | 1% | 1% | 2% |

| 3% | 1% | 3% | 4% |

| 5% | 1% | 4% | 5% |

The beauty of this? Even if you only serve 4 years, you get to keep all that government money. Under High-3, you’d walk away with nothing.

Key BRS Features and Financial Risks (The Stuff That Could Bite You)

Alright, now let’s talk about some of the features of BRS that sound good on paper but can actually cost you big time if you’re not careful.

The Lump Sum Benefit: Why It Costs You More (Spoiler Alert: It’s a Trap)

So BRS has this option that sounds tempting—like, really tempting when you’re staring at retirement and thinking about all the things you could do with a big chunk of cash right now.

What’s the option? When you retire under BRS, you can choose to take a lump sum payment of either 25% or 50% of your estimated military retirement pay. Just imagine—tens or even hundreds of thousands of dollars dropped in your bank account the day you retire.

The catch (because there’s always a catch): If you take that lump sum, your monthly retirement check gets slashed until you hit 67 years old. Then—and only then—does it go back to the full amount.

The financial penalty (this is where it gets ugly): The military uses something called the Lump Sum Discount Rate (LSDR) to figure out your lump sum. For retirements in 2026, that rate is 6.46%. What does that mean? It means you’re getting way less money than you should. They’re basically making you pay interest to get your own money early.

Real-world example from 2026 (prepare to cringe): Let’s say you’re an O-5 (Lieutenant Colonel) who retires at age 42 in 2026. You’re making $12,032.80 per month in basic pay. Under BRS, your pension would be 40% of that, or $4,813.12 per month for life.

Now, if you take a 25% lump sum, you might get a check for about $137,100 upfront. Sounds awesome, right? Wrong.

Over the next 25 years (until you’re 67), the total reduction in your monthly payments will exceed $274,500. You read that right—you’re paying a $137,000+ premium just to get your own money early. That’s basically borrowing from yourself at a 6.46% interest rate, except worse because you’re also losing all the COLA adjustments on that missing money.

For an E-8, the numbers are still brutal. Over 29 years, you could lose hundreds of thousands of dollars. For that O-5, it’s over half a million dollars over 25 years. That’s more than half a million dollars you’re kissing goodbye!

Tax impact (it gets worse): That lump sum isn’t tax-free, my friend. It counts as income for that year, which could bump you into a higher tax bracket. Suddenly you’re paying 24% or even 35% in taxes instead of 12% or 22%. An O-5 taking a 50% lump sum could see 50,000-\70,000 vanish just in federal taxes that first year.

The Only Scenario Where It Might Make Sense:

The DoD Office of the Actuary isn’t stupid—they priced this to benefit the government, not you. For the lump sum to work in your favor, you’d need to:

- Invest it immediately and earn more than 6.46% after taxes every single year

- Beat the compounding effect of the COLA adjustments you’re giving up

- Not spend a penny of it for 25 years

Yeah, good luck with that.

Bottom line: This option is designed to save the government money, not you. Unless you have some really specific reason to need that cash NOW—and I mean really specific, like paying off predatory debt with 10%+ interest—don’t do it. Just don’t. When you estimate military retirement pay, always run the numbers with and without the lump sum to see the real cost.

Continuation Pay (CP) (Free Money for Sticking Around)

Here’s something that’s actually a nice perk of BRS, but there are important updates for 2026:

When you get it: When you hit your mid-career mark (between 8-12 years depending on your service) and commit to additional years, the military throws you a bonus called Continuation Pay. Think of it as the DoD saying “hey, we really want you to stick around.”

2026 CHANGES – CRITICAL FOR ALL SERVICES:

Army Changes (Active and Guard/Reserve):

- Army Active Duty: The eligibility window expands in 2026 to those with 7-12 years of service (previously 8-12 years). This is huge—if you’re approaching year 7, you can now lock in your CP a year earlier.

- Army National Guard M-Day (Drilling Status) Guardsmen: The CP multiplier is dropping dramatically from 2.5x to just 0.5x your monthly active duty base pay starting January 1, 2026. That’s a difference of over $9,000 for an E-6 with 10 years!

- Exception for Mobilized Guardsmen: If you’ve served 270+ days of involuntary mobilization within a 730-day window, you still qualify for the 2.5x multiplier

- AGR Soldiers: No change—CP remains at 2.5x monthly base pay

Marine Corps (Still the Most Generous):

- Active / Active Reserve: 5.0x multiplier (highest in DoD)

- Reserve (SMCR/IMA): 1.0x multiplier

Navy, Air Force, Space Force:

- Active components maintain 2.5x multipliers

- Reserve components generally at 0.5x (Navy Selected Reserve confirmed at 0.5x)

How much we talking? Let’s break down some real 2026 numbers:

E-7 with 10 years (Master Sergeant/Gunnery Sergeant):

- 2026 monthly basic pay: $5,300.34

- Army Active (2.5x): $13,250.85

- Marine Corps Active (5.0x): $26,501.70

- Army Guard Drilling (0.5x): $2,650.17

O-3 with 8 years (Captain):

- 2026 monthly basic pay: $8,251.50

- Most Active Duty (2.5x): $20,628.75

- Marine Corps Active (5.0x): $41,257.50

URGENT: If you’re close to the 7-12 year mark:

Act now if you’re currently eligible. Soldiers who qualify for CP under the 2025 rates can still sign their agreement before the policy change takes effect on January 1, 2026. The Army’s expansion to year 7 is projected to contract back to 7-10 years by 2027, so there’s a narrow window here.

Reach out to your Career Counselor, State Incentive Manager, or HR professional to understand your eligibility and options.

Combat Zone Tax Exclusion (CZTE) Bonus:

If you receive your Continuation Pay while serving in a designated combat zone, the entire bonus may be tax-exempt. This is massive—it’s like getting a 12% to 37% raise on that bonus depending on your tax bracket. Smart service members use this window to pump that money straight into their Roth TSP, getting the tax break on both ends.

This is basically the military saying “thanks for committing to stick around.” Unlike the lump sum option, this one doesn’t cost you anything in the long run—it’s pure bonus money.

Retirement for National Guard and Reserves (Because You’re Part of the Team Too)

If you’re Guard or Reserve, the retirement rules work a little differently—but don’t worry, you still get to retire!

Eligibility: You need 20 qualifying years of service. But here’s the thing—a “qualifying year” for Guard and Reserve means you earned at least 50 retirement points that year.

How the defined benefit works: They use the same 2% multiplier formula for BRS (or 2.5% if you’re under High-3), but they have to calculate your “equivalent years” of active service because you’re not serving full-time.

When you actually get paid: This is the big difference. For most Guard and Reserve folks, military retirement pay doesn’t start until you’re 60 years old. However, if you’ve done active service since 2018, you might qualify to start as early as age 50. Every 90 days of active service knocks your retirement age down by three months.

How they calculate it (the points system): Every drill weekend, annual training, and active duty stint earns you retirement points. When it’s time to retire, they divide your total points by 360 to figure out your equivalent years of service. So if you have 7,200 points, that’s 20 years’ worth.

The “gray area”: This is what they call the time between when you retire from the Guard/Reserve and when you actually start getting paid. Fun fact: your longevity for pay purposes keeps counting during this time, which means when you do start getting paid, it’ll be based on the current pay scale, not the one from when you retired.

Critical TSP Rules & Investment Strategy (Don’t Screw This Up)

Your TSP is a huge part of your military retirement under BRS, so let’s talk about how to not mess it up.

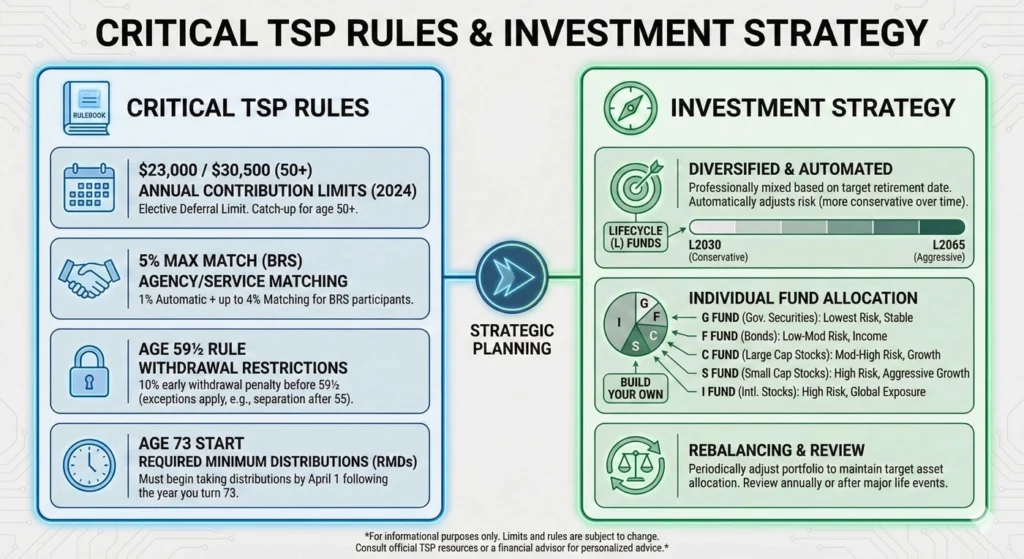

2026 TSP Contribution Limits (UPDATED!)

The big news: The TSP contribution limit for 2026 is $24,500, up from $23,500 in 2025. This is the elective deferral limit—the maximum you can contribute from your own pay.

Catch-up contributions (age 50+): An additional $8,000 in catch-up contributions (up from $7,500 in 2025), bringing your total to $32,500.

Super catch-up (ages 60-63): If you’re between 60 and 63, you get an even higher catch-up limit of $11,250 instead of $8,000, bringing your total to $35,750. This is a huge opportunity if you’re in this age range! This comes from SECURE Act 2.0 and is designed to help people in their final working years really supercharge their retirement savings.

NEW 2026 Rule – High Earners: If you earned more than $150,000 in 2025 and you’re 50 or older in 2026, your catch-up contributions MUST be Roth. This happens automatically—your payroll office handles it for you. This mainly affects O-5s and above, and senior enlisted (E-9s) with specialty pays.

Annual additions limit: Military matching contributions don’t count toward the $24,500 limit; they count toward the separate $72,000 annual additions limit for 2026.

Combat zone contributions: Service members deployed to combat zones can contribute up to the full $72,000 annual additions limit from tax-exempt pay. This is a massive wealth-building opportunity if you’re deployed!

NEW 2026: Roth In-Plan Conversions

Starting late January 2026, the TSP launched “Roth In-Plan Conversions.” This is a game-changer for strategic retirement planning.

What it is: You can now move money from your traditional (pre-tax) TSP balance into your Roth (post-tax) TSP balance, all within the same account. You’ll pay income tax on the amount you convert, but then that money and all its future growth can be withdrawn tax-free in retirement.

Why this matters: Let’s say you’re an E-6 right now but you expect to retire as an E-8 with a decent pension. You might be in the 12% tax bracket now but could be in the 22% bracket in retirement. By converting some traditional TSP to Roth now, you pay 12% tax today to avoid 22% tax in retirement. That’s a 10% arbitrage opportunity.

Strategic conversion timing:

- Do it in years when your income is lower (like right after you separate before starting a civilian job)

- Do it when the market is down (convert more shares for the same tax bill)

- Spread it over multiple years to avoid bracket creep

When you can actually touch the money

You can’t withdraw from your TSP without a penalty until you’re 59½ or 60. If you try to pull it out early, you’re getting hit with a 10% tax penalty on top of regular income taxes. There are some exceptions for extreme circumstances and fancy withdrawal strategies (like SEPP), but generally speaking, that money’s locked up until you’re close to 60.

Investment risk (the double-edged sword)

Unlike your pension, which is guaranteed, your TSP is invested in the market. That means it can grow like crazy—or it can shrink. Historical data shows the C Fund (which tracks the S&P 500) has returned about 10-11% annually over the long term, but that includes some years where it dropped 30-40%.

The G Fund Mistake (seriously, don’t do this)

If you’re still serving and your TSP money is sitting in the G Fund, you need to change that like, yesterday. The G Fund is the “safe” option—it’s basically government bonds—but “safe” also means “barely growing.” In 2026, the G Fund is paying around 4-5%, which sounds okay until you realize inflation is eating 2.8% of that, leaving you with only 2% real growth.

Over 20 or 30 years, you’re leaving massive amounts of money on the table. Check this out:

20-Year TSP Growth Comparison (contributing $500/month):

- G Fund only (4% return): ~$183,000

- C Fund only (10% return): ~$382,000

- Difference: $199,000 you left on the table

The C Fund (tracks the S&P 500) and I Fund (international stocks) have way higher growth potential. Yeah, they’re riskier, but when you’ve got decades until retirement, you have time to ride out the market ups and downs. The younger you are, the more aggressive you can be. A common strategy is to go heavy on C and I Funds early, then gradually shift to more conservative funds as you get closer to retirement.

THE BRS MATCH TRAP – Don’t Max Out Too Early!

CRITICAL MISTAKE: If you’re in BRS and you max out your TSP in July, you’ll get NO MATCH for August through December. Why? Because matching is paid on a per-pay-period basis—you must contribute at least 5% EVERY month to receive that month’s match.

The solution: Calculate your percentage to hit exactly $24,500 in December, not before.

Here’s the math for 2026:

E-6 with 8 years:

- Monthly basic pay: $3,958 (with 3.8% raise)

- Annual basic pay: $47,496

- To max out in December: $24,500 ÷ $47,496 = 51.6%

- Set your TSP to 52% to capture the full year of matching

O-4 with 12 years:

- Monthly basic pay: $9,360

- Annual basic pay: $112,320

- To max out in December: $24,500 ÷ $112,320 = 21.8%

- Set your TSP to 22%

If you max out early, you’re literally walking away from thousands of dollars. For that E-6, missing 5 months of matching at 5% means losing about $990. For the O-4, it’s about $2,340. That’s real money you’re leaving on the table.

Think about it—if your military retirement estimator shows you’re going to get 40% of your base pay as a pension, that TSP might need to make up the difference if you want to maintain your lifestyle in retirement.

Maximizing Financial Health: Avoiding Common Pension Estimate Mistakes (Because Errors Happen)

Let’s talk about how to make sure you’re not getting screwed on your estimates—either by accident or by someone not doing their job right.

Verify everything: Those agency estimates you get? They’re only as accurate as the data someone typed in. And guess what? People make mistakes. I’ve seen estimates that were off by tens of thousands of dollars.

Know your Official Personnel Folder (OPF): This is where all your career data lives. Your agency and the Office of Personnel Management (OPM) use this to calculate your pension. You need to know how to access it and check it regularly. Think of it as your military/federal resume that determines your paycheck for the rest of your life.

Review your SF-50s: These are your official personnel action forms. Check the effective date of your very first SF-50 to make sure they’re counting all your creditable service. Every time you changed positions or agencies, there should be an SF-50. If one’s missing, your service might not be counted correctly.

Watch out for these service types:

- Temporary service might not count

- Intermittent service has special rules

- If you bought back military service time for your civilian retirement, make sure it’s documented so you don’t end up paying twice

- Leave without pay for more than six months in a calendar year might not count toward retirement

Coverage continuity (the 5-year rule): If you want to keep your FEHB (health insurance) and FEGLI (life insurance) in retirement, you MUST be covered for the five years immediately before you retire. Don’t let this lapse, or you’ll lose the option to keep these benefits.

Calculate your NET pension: Here’s a mistake I see all the time—people look at their gross pension estimate and start making retirement plans. But that’s before taxes, before your health insurance premiums, before survivor benefit payments, before everything. Your actual take-home (net) pension could be 20-30% less than the gross number. Always calculate what you’ll actually have hitting your bank account every month. When you estimate military retirement pay, the net number is what really matters.

Real-World Case Studies: Who Wins Under Each System?

Let’s stop talking theory and look at actual numbers for real service members retiring in 2026.

Case Study #1: E-7 Enlisted Retiree (Master Sergeant)

Meet Sarah, an Army Master Sergeant who’s retiring in 2026 with exactly 20 years of service. She’s 42 years old and is trying to figure out what her retirement will actually look like.

2026 Pay: E-7 with 20 years earns $6,245.70 per month in basic pay.

Scenario A: High-3 System

- Pension multiplier: 50% (2.5% × 20 years)

- Monthly pension: $3,122.85

- Annual pension: $37,474

- TSP balance: Maybe 50,000-\100,000 if she contributed on her own (no matching)

- Continuation Pay received: $0 (not part of High-3)

Scenario B: BRS

- Pension multiplier: 40% (2.0% × 20 years)

- Monthly pension: $2,498.28

- Annual pension: $29,979

- Monthly gap vs. High-3: $624.57

- TSP balance: Approximately 180,000-\220,000 (assuming she maxed the 5% match for 18 years)

- Continuation Pay received: 13,250atyear10(whichifinvestedat726,000)

The Breakeven Analysis:

At first glance, Sarah’s taking a $624.57 monthly hit under BRS. That’s $7,495 per year. Over a 40-year retirement, that’s roughly $300,000 in pension payments she’s “losing.”

But here’s what she gained:

- Government-contributed TSP: ~$200,000

- Continuation Pay growth: ~$26,000

- Total extra assets: ~$226,000

At a conservative 4% withdrawal rate, that $226,000 generates about $753 per month—which actually exceeds the $624.57 pension gap!

The Verdict: For Sarah who made it to 20 years, it’s basically a wash financially. High-3 gives slightly more guaranteed income, but BRS gives her a $226,000 nest egg she can pass to her kids. If Sarah had left at year 12 due to an injury, High-3 would have given her $0, while BRS would have given her about $85,000 in TSP.

Case Study #2: O-5 Officer Retiree (Lieutenant Colonel)

Meet James, an Air Force Lieutenant Colonel retiring in 2026 with 20 years of service. He’s 44 years old, and unlike Sarah, the numbers hit differently for officers.

2026 Pay: O-5 with 20 years earns $12,032.80 per month in basic pay.

Scenario A: High-3 System

- Monthly pension: $6,016.40 (50%)

- Annual pension: $72,197

- TSP balance: Maybe 150,000-\250,000 from personal contributions (no matching)

Scenario B: BRS

- Monthly pension: $4,813.12 (40%)

- Annual pension: $57,757

- Monthly gap vs. High-3: $1,203.28

- TSP balance: Approximately 280,000-\350,000 (maxed the 5% match consistently)

- Continuation Pay: ~$52,000 invested at year 10

The Breakeven Analysis:

James is looking at a $1,203.28 monthly gap—that’s $14,439 per year. Over 40 years, that’s a whopping $577,560 in pension payments he’s giving up. This is where being an officer makes a difference—the 10% pension cut hurts more in absolute dollars.

To make up that gap with his TSP:

- He needs his TSP to generate $1,203.28/month

- At 4% withdrawal rate, he’d need $361,000 in TSP

- His government-match portion is about 280,000-\350,000

- Plus Continuation Pay growth of ~$100,000

The Verdict: For James, the BRS comes close but doesn’t quite make up the full difference if he’s looking purely at income. However, here’s what swings it:

- Longevity: Officers typically live longer (higher education correlates with longer life expectancy). James might collect that pension for 45+ years, making the guaranteed inflation-adjusted income of High-3 more valuable.

- Legacy: That $350,000+ TSP balance is inheritable. His High-3 pension dies with him (unless he elected Survivor Benefit Plan, which costs 6.5% of his pension).

- Safety net: If James had been forced out at year 15 due to a RIF (Reduction in Force), High-3 gives him $0. BRS gives him $180,000+ in TSP.

For officers certain they’ll make 20 years, High-3 is mathematically superior. But for officers who face the uncertainty of promotion boards, medical issues, or force reductions, BRS provides critical insurance.

Case Study #3: The Person Who Doesn’t Make It to 20 (The 80% Scenario)

Meet Marcus, an E-5 Sergeant who joined in 2015 under High-3 and separated in 2026 after 11 years of service due to a family emergency.

High-3 Result:

- Pension received: $0

- TSP balance: ~$35,000 (from personal contributions only, no matching)

- Continuation Pay: $0 (not part of High-3)

- Total retirement assets: $35,000

Now imagine Marcus had been under BRS:

BRS Result:

- Pension received: Still $0 (didn’t make 20 years)

- TSP balance: ~$85,000 (government matching added $50,000+ over 9 years)

- Continuation Pay: $10,600 received at year 8

- Total retirement assets: $95,000+

The Verdict: For the 81% of service members who don’t make it to 20 years, BRS is a complete game-changer. Marcus walking away with $95,000 versus $35,000 is the difference between having a down payment for a house and… not.

This is why DoD created BRS—to provide retirement benefits to the majority of service members, not just the 19% who stay for a full career.

2026 Military Pay and COLA Increases

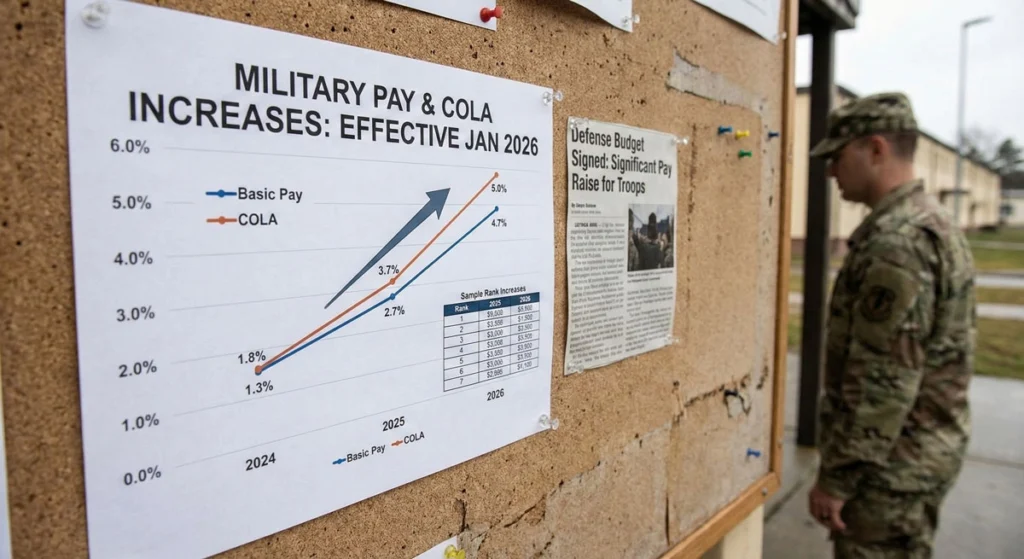

Active Duty Pay Raise: Military service members received a 3.8% pay raise in 2026. While this is lower than the exceptional 4.5-5.2% raises of 2023-2025, it exceeds historical averages and maintains purchasing power.

Retiree COLA: Military retirees received a 2.8% cost-of-living adjustment (COLA) in 2026, up from 2.5% in 2025. This increase applied to retired pay starting with December 2025 entitlements (typically deposited around January 1, 2026).

REDUX Retirees: If you’re under the REDUX retirement system (took the Career Status Bonus at 15 years), your COLA is CPI minus 1 percentage point. For 2026, REDUX retirees received a 1.8% COLA instead of 2.8%.

Example impact: An E-7 retiree receiving $31,900/year pension would see it increase to $32,793/year with the 2.8% COLA—an extra $893 annually.

State Tax Planning: Where You Retire Matters (A Lot)

Here’s something most people don’t think about until it’s too late: where you live in retirement can cost or save you tens of thousands of dollars. As of 2026, state taxation of military retirement pay varies wildly, and it’s a primary driver of where retirees choose to live.

2026 State Tax Categories for Military Retirement:

No State Income Tax (The Winners):

- Florida, Texas, Nevada, Washington, Wyoming, South Dakota, Tennessee, Alaska, New Hampshire

- Impact: Every dollar of your pension is yours. Every dollar you withdraw from your TSP is yours. This effectively increases your net retirement income by 4-9% compared to states that tax it.

- Popular retiree destinations: Florida (1.1 million veterans), Texas (1.6 million veterans)

Full Military Retirement Exemption (The Smart Movers):

- Georgia, North Carolina, South Carolina, Indiana, Nebraska, Ohio, Alabama, Illinois, Mississippi

- Impact: Your military pension is completely tax-free, but TSP withdrawals and other income are still taxed. Still, this is hugely competitive for retirees.

- Example: An E-7 retiree with a $3,122 monthly pension saves about 1,800-\2,800 annually compared to states that tax it.

Partial Exemptions (The “Meh” States):

- Delaware: $12,500 exclusion (covers most junior enlisted pensions)

- Colorado: $15,000 exclusion for those 55-64, $20,000 for 65+

- Impact: Benefits lower-rank retirees (E-6 and below) more than officers.

Full Taxation (The Expensive States):

- California, Vermont, Washington D.C., and several others

- Impact: Your military pension is taxed as regular income.

California 2026 Update:

California remains one of the few states to fully tax military retirement pay, though it has introduced a limited exclusion of up to $20,000 for surviving spouses or those with adjusted gross income below $250,000.

For our O-5 James retiring with 6,016monthlypension(72,197 annually), California state tax at 9.3% would cost him about 6,714 per year**. Over a 40-year retirement, that’s **\268,560 in state taxes that he wouldn’t pay in Texas or Florida.

Real-World Impact on Retirement Planning:

Let’s compare that E-7 Sarah’s retirement in different states:

Sarah’s Annual Pension: $37,474 (High-3)

| State | State Tax Rate | Annual Tax Bill | 40-Year Cost |

|---|---|---|---|

| Texas | 0% | $0 | $0 |

| Florida | 0% | $0 | $0 |

| Georgia | 0% (exempt) | $0 | $0 |

| Colorado | ~3% (after $20k exemption) | ~$523 | ~$20,920 |

| California | 6% (her bracket) | ~$2,248 | ~$89,920 |

That’s potentially $90,000 in savings just by choosing the right state. When you’re using a military retirement estimator, always run the net numbers for where you actually plan to live.

Combat Zone Tax Exclusion (CZTE) Strategies for 2026

For members currently deployed or about to deploy to designated combat zones, the CZTE creates powerful wealth-building windows that you need to exploit.

What’s Tax-Exempt in Combat Zones:

- All basic pay (for enlisted and warrant officers)

- For officers: Up to the highest enlisted pay ($9,857.40/month in 2026)

- Hostile fire pay / imminent danger pay

- Reenlistment bonuses (if signed in the combat zone)

- Continuation Pay (if received while in zone)

The BRS/CZTE Super Strategy:

If you’re approaching your Continuation Pay eligibility and you know you’ll be deployed, try to time it so you receive your CP while boots-on-ground in a combat zone.

Example:

An E-7 receiving $13,250 in Continuation Pay while deployed:

- Normal scenario: Pays ~2,500-\3,500 in federal taxes (22% bracket)

- CZTE scenario: Pays $0 in federal taxes

- Savings: 2,500-\3,500

Then, take that entire $13,250 and dump it into your Roth TSP. Why? Because:

- You already got the tax break on the front end (CZTE)

- It grows tax-free in the Roth

- You withdraw it tax-free in retirement

- You just created $13,250 of wealth that will never be taxed, ever

If that $13,250 grows at 7% for 20 years, it becomes 51,800—completelytax−free.Inanormalscenario,youmightpay228,500 in taxes). You just saved $11,000 by timing one decision correctly.

2026 Combat Zone TSP Contributions:

Remember that $72,000 annual additions limit? In combat zones, you can contribute your entire tax-exempt pay up to that limit into your TSP. For enlisted members making 4,000-\6,000/month, this means you could potentially sock away 48,000-\72,000 in a single deployment year.

Real scenario: An E-6 on a 12-month deployment making $4,500/month in tax-exempt pay:

- Can contribute: $54,000 to TSP for that year

- Normal limit without deployment: $24,500

- Extra wealth-building: $29,500

If you’re 25 years old and that $29,500 grows at 7% until you’re 60, it becomes $320,000. From one deployment. This is the single biggest wealth-building opportunity in military service.

The Strategic Advantage of BRS in 2026: Final Analysis

After diving into all these numbers, case studies, and scenarios, here’s the bottom line:

1. Portable Equity (The Game-Changer for Most People)

In an era where the average American changes jobs 12 times in their career, the military can’t expect 100% of recruits to stay for 20 years. The BRS acknowledges this reality.

A Captain or Staff Sergeant separating at year 8 walks away with 50,000-\100,000 in TSP wealth under BRS, versus $0 under High-3. That’s not just retirement money—that’s a house down payment, a business startup fund, or a college fund for their kids.

2. Mid-Career Liquidity (When You Need It Most)

The Continuation Pay multipliers in 2026 (2.5x to 5.0x depending on service branch) provide significant capital at exactly the time when many service members are buying homes, starting families, or dealing with the financial pressures of being NCOs or junior officers.

For a Marine E-7, that 5.0x multiplier means $26,501—that’s real money that can change your family’s financial trajectory. And unlike the lump sum retirement option, this doesn’t cost you anything long-term.

3. Tax-Efficient Growth (The Hidden Advantage)

The introduction of Roth In-Plan Conversions in 2026, combined with the combat zone tax exclusion opportunities, allows service members to build substantial tax-free wealth. This is a wealth-preservation tool that significantly offsets the lower 2.0% pension multiplier.

Over a 30-40 year retirement, having 300,000-\500,000 in Roth TSP (completely tax-free) versus traditional TSP (fully taxable) could save you 75,000-\150,000 in taxes. That’s real money that makes up for a lot of that pension difference.

For the “Lifer”—Still Some Math in Favor of High-3:

If you are absolutely certain you’re staying for 20+ years, started your career early (before age 25), and want maximum guaranteed income, the High-3 system remains the “gold standard” due to the 2.5% multiplier. The guaranteed, inflation-adjusted annuity with no market risk is valuable, especially for:

- Officers who will have substantial pensions (O-4 and above)

- Those with family longevity (expecting to collect for 35-40+ years)

- Conservative investors who don’t want market risk

- People who value simplicity over portfolio management

But for the 81% Who Don’t Make It to 20 Years:

The BRS is the clear, undisputed winner. It provides structural benefits that the High-3 simply doesn’t offer. Even for those who do make it to 20 years, the flexibility, inheritance value, and tax advantages of the TSP component make BRS far more resilient for modern military families.

The Rising Cost of Retiree Healthcare (Because Nothing Stays Cheap Forever)

Real talk: your healthcare costs are going up. They go up pretty much every year, and you need to factor this into your military retirement planning.

2026 Tricare Cost Increases (UPDATED!)

Most Tricare Prime and Select users will see increases of about 2-3% in copays, premiums, and other payments in 2026. However, some premium-based plans saw steeper increases:

2026 Annual Enrollment Fees (examples):

- Group A retiree individuals on Tricare Prime: $381.96 per year (up from $372 in 2025)

- Group B retiree families on Tricare Prime: $900.96 per year

Deductibles (2026):

- Group B families (E-5 and above) on Tricare Select: Family deductible increased from $386 to $397

- Group B individuals (E-5 and above) on Tricare Select: Individual deductible increased from $193 to $198

Catastrophic Caps (2026):

- Group A retirees using Tricare Select: $4,381 (up from $4,261 in 2025)

- Group B retirees using Tricare Select: $4,635 (up from $4,509 in 2025)

Premium-Based Plans (Bigger Increases):

These plans saw significant increases in 2026:

- Tricare Reserve Select:

- Member only: $57.88/month (up from $53.80)

- Member and family: $286.66/month (up from $274.48)

- Tricare Retired Reserve:

- Member only: $645.90/month (up from $631.26)

- Member and family: $1,548.30/month (up from $1,513.04)

- Tricare Young Adult (ages 21-26):

- Prime: $794/month (up 9.2% from $727)

- Select: $363/month (up 7.7% from $337)

- Continued Health Care Benefit Program (CHCBP):

- Member only: $2,103/quarter (up from $1,849)

- Family: $5,339/quarter (up from $4,621)

What determines your costs? You’re in either Group A (entered service before January 1, 2018) or Group B (entered on or after January 1, 2018). Generally, Group B pays more.

Why am I telling you all this? Because when you’re using a military retirement estimator to plan your future, you need to account for healthcare costs. They’re not optional, and they’re not going to get cheaper. Build them into your budget from day one.

Next Steps and Trusted Resources (Time to Actually Do Something)

Alright, so you’ve read all this—now what? Here’s what you need to do:

Calculate your options: Stop guessing and get real numbers. Head over to the official DoD BRS Comparison Calculator at https://militarypay.defense.gov/Calculators/BRS. They’ve also got High-3 and Final Pay calculators. Plug in your actual information and see what your military retirement could look like under each system.

Play around with different scenarios. What if you retire at 20 years vs. 22 years? What if your TSP returns average 7% vs. 9%? What if you take the lump sum vs. don’t? Run all the numbers so you know exactly what you’re looking at.

Get professional help (the free kind): Military OneSource offers free financial counseling. These folks can sit down with you (virtually or in person) and walk through your estimates. They’ve seen thousands of service members’ situations, and they can spot issues you might miss.

Check out FINRED: The Office of Financial Readiness has tons of resources at https://finred.usalearning.gov. We’re talking articles, calculators, courses—everything you need to make smart financial decisions about your military retirement.

Talk to people who’ve done it: Find someone who’s recently retired under the system you’re considering. Buy them coffee and pick their brain. What do they wish they’d known? What would they do differently? Real-world experience is invaluable.

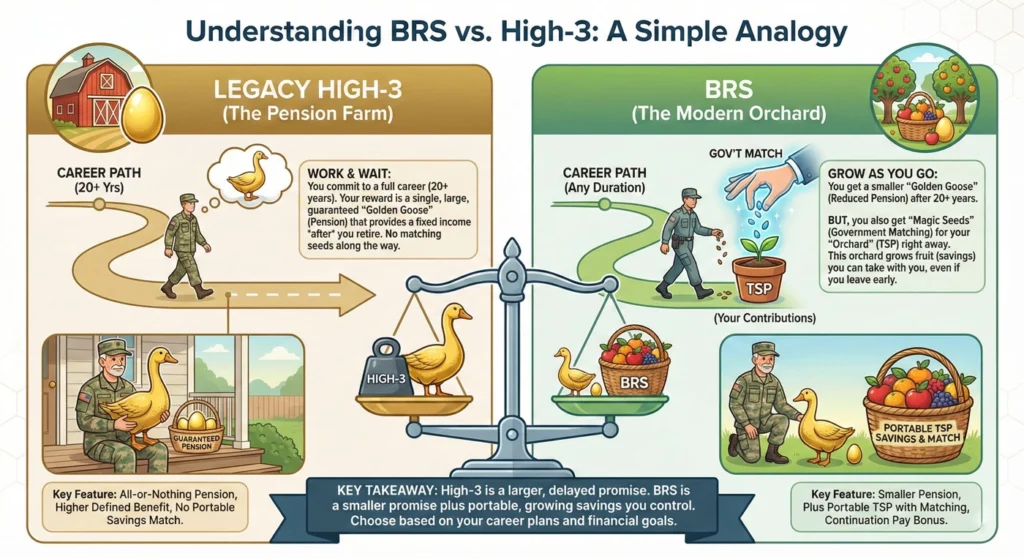

Understanding BRS vs. High-3: A Simple Analogy

Still confused? Let me break it down with an analogy that’ll make this crystal clear.

Choosing between BRS and High-3 is like picking between two vehicles for a 20-year cross-country road trip:

High-3 is like a reliable, high-mileage bus. It only completes the trip if you stay on board for the entire 20 years—no exceptions. If you jump off at year 15? Too bad, you get nothing. But if you stick it out and stay on that bus for the full ride, you get a big, comfortable monthly paycheck (your pension) for the rest of your life. It’s predictable, it’s stable, and it’s substantial—50% of your pay, inflation-adjusted, guaranteed by the U.S. government. The bus might not be exciting, but man, it gets you where you need to go with maximum comfort.

BRS is like a hybrid car with a growing investment account. It’s got a reliable gas engine (that 40% pension) that’ll get you there, but it’s a bit smaller than the bus engine. However—and here’s where it gets interesting—every single month you’re on the journey, the car hands you actual cash (that 5% TSP match) that you can invest in building up your own secondary vehicle. If something happens and you have to exit the trip early at year 10, you don’t lose everything. You keep that growing investment and all the money you’ve built up in it—maybe 75,000-\100,000 of real, portable wealth.

But here’s the warning: if you get tempted by that lump sum option and take a bunch of quick cash upfront, you’re basically depleting the gas tank of your primary engine. Sure, you’ve got money in your pocket right now, but you’re going to be crawling along real slow in your later years until age 67. By then, you’ve already lost years of comfortable cruising and literally hundreds of thousands of dollars.

Which vehicle would I choose?

Honestly, it depends on your plans and your situation:

Choose High-3 if:

- You’re 100% certain you’re doing the full 20 years

- You started early (before age 25)

- You’re already at 10+ years under High-3

- You want maximum guaranteed income

- You don’t want to think about investments

Choose BRS if:

- There’s any doubt about making it to 20 years

- You value flexibility and portability

- You’re comfortable managing investments

- You want to build inheritable wealth

- You’re in a high-deployment/high-risk career field

- You’re early in your career (under 7-8 years)

For Guard and Reserve:

BRS is almost always the better call because the likelihood of accumulating a full 20 qualifying years is statistically lower, and you want to make sure you’re building that TSP account regardless of what happens. Plus, with the 2026 Continuation Pay cuts for drilling Guard members (2.5x down to 0.5x), you need every advantage you can get—that TSP match becomes even more critical.

The 13-Year Inflection Point:

Financial modeling shows that if you’re planning to stay for 20+ years, there’s a “breakeven” point at around 13 years of service. If you’re past 13 years under High-3, the math strongly favors staying with High-3. If you’re under 8 years, BRS gives you better lifetime value in most scenarios. In between? It’s a judgment call based on your personal situation.

Final Thoughts: Your Retirement, Your Choice

Look, military retirement is one of the best benefits out there. Whether you’re looking at High-3 or BRS, you’re building something that most Americans don’t have—a guaranteed income stream in retirement. Only about 14% of private-sector workers have a traditional pension anymore. You’re in an elite club.

But here’s the thing: you’ve got to actually plan for it. Use that military retirement estimator. Run the numbers. Be honest with yourself about whether you’re really going to do 20 years or not. Talk to your spouse or partner about what retirement looks like for your family. Max out that TSP match if you’re under BRS—seriously, it’s free money.

2026 Action Items:

✅Update your TSP contributions to account for the new $24,500 limit

✅ Calculate your monthly contribution percentage to hit $24,500 in December (not before!) if you’re in BRS

✅ Check if you’re eligible for Continuation Pay before the January 1, 2026 policy changes (especially Army and Guard members!)

✅ Review your 2026 Tricare costs and adjust your budget accordingly

✅ Consider Roth in-plan conversions if you’re in a low tax year

✅ Explore the super catch-up contributions if you’re ages 60-63 ($11,250 instead of $8,000)

✅ Run your numbers through the official DoD calculator at militarypay.defense.gov

✅ If you’re deployed, maximize your combat zone tax exclusion strategies

And whatever you do, don’t take that lump sum unless you’ve run the numbers with a financial advisor and you have a really, really good reason. I can’t stress this enough—it looks tempting, but the math almost never works out in your favor. In our case studies, we saw people losing 200,000-\500,000 over their lifetime. That’s generational wealth you’re throwing away.

Your military service is valuable. Your retirement should reflect that. So take the time to understand your options, make an informed choice, and set yourself up for a comfortable future. You’ve earned it.

Remember:

- High-3 gives you maximum guaranteed income if you make it to 20

- BRS gives you something valuable even if life throws you a curveball

- The TSP match under BRS is literally free money—take it

- State taxes can cost you six figures over retirement—plan accordingly

- Combat zone deployments are wealth-building super-opportunities

- The lump sum option is almost always a trap

Now get out there and start planning. Your future self will thank you.

Last updated: February 2026. Information reflects the latest changes to military pay (3.8% raise), retiree COLA (2.8%), TSP contribution limits ($24,500), Tricare costs, Continuation Pay policy changes effective January 1, 2026, and the introduction of Roth In-Plan Conversions.